“I have found that the importance of having an investment philosophy—one that is robust and that you can stick with— cannot be overstated.” —David Booth

The US stock market has delivered an average annual return of around 10% since 1926.1 But short-term results may vary, and in any given period stock returns can be positive, negative, or flat. When setting expectations, it’s helpful to see the range of outcomes experienced by investors historically. For example, how often have the stock market’s annual returns actually aligned with its long-term average?

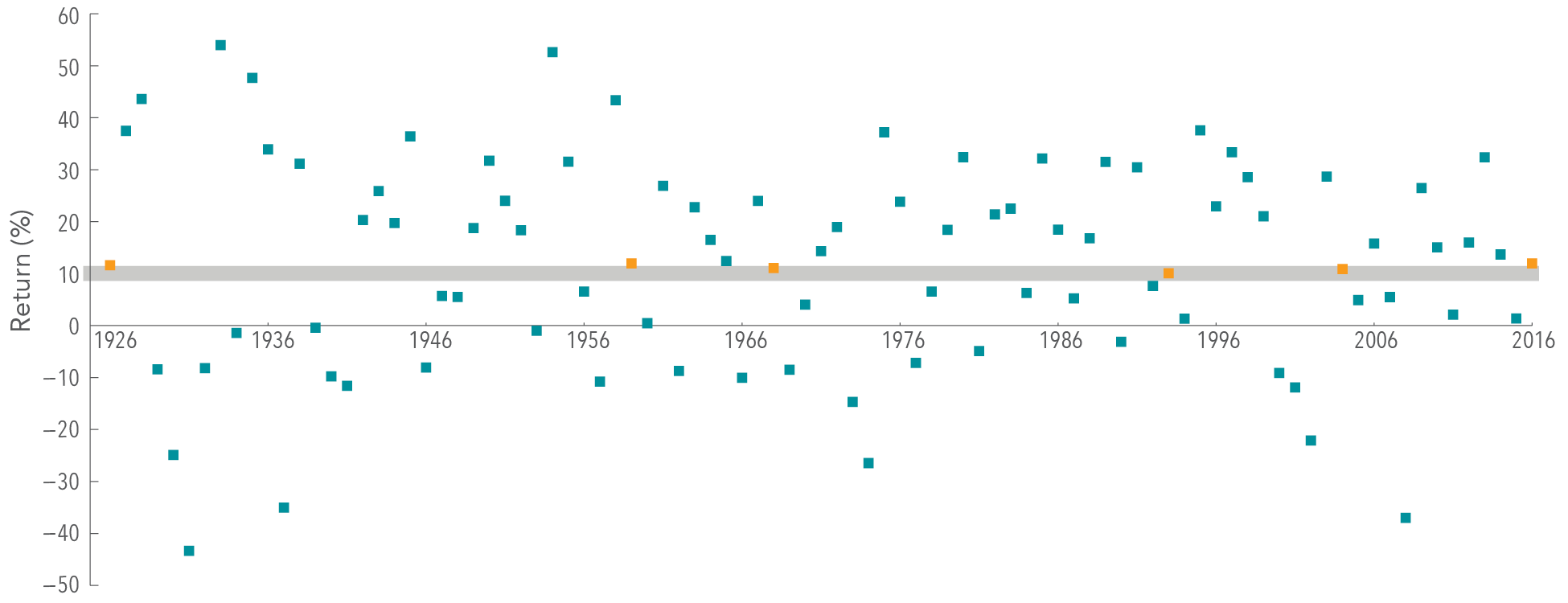

Exhibit 1 shows calendar year returns for the S&P 500 Index since 1926. The shaded band marks the historical average annual return of 10%, plus or minus 2 percentage points. The S&P 500 had a return within this range in only six of the past 91 calendar years. In most years the index’s return was outside of the range, often above or below by a wide margin, with no obvious pattern. For investors, this data highlights the importance of looking beyond average annual returns and being aware of the range of potential outcomes.

TUNING IN TO DIFFERENT FREQUENCIES

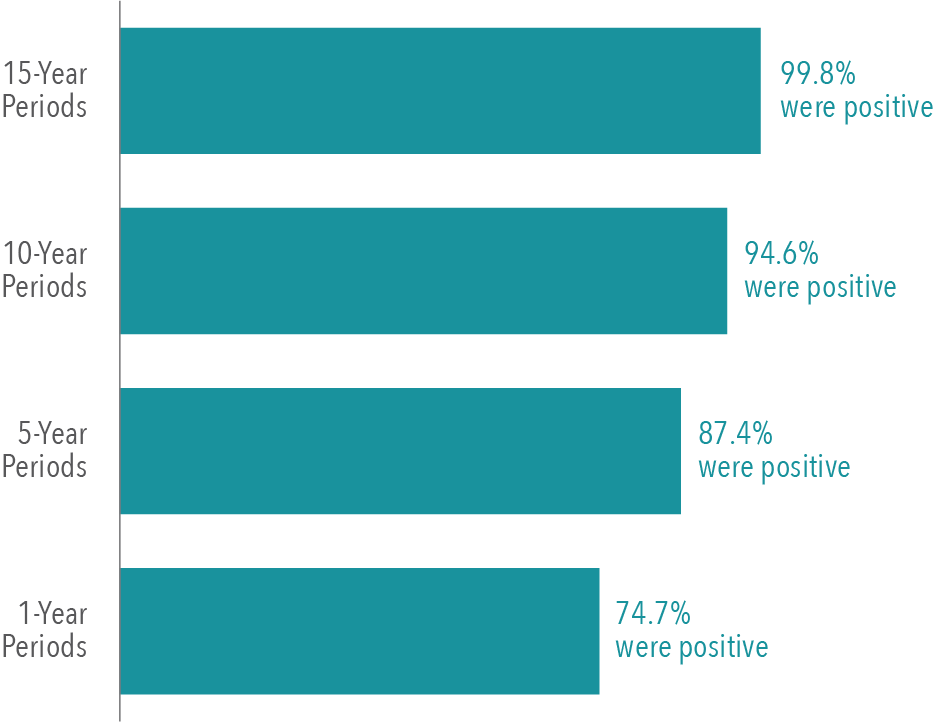

Despite the year-to-year uncertainty, investors can potentially increase their chances of having a positive average annual return outcome by maintaining a long-term focus. Exhibit 2 documents the historical frequency of positive returns over rolling periods of one, five, 10, and 15 years in the US market. The data shows that, while positive performance is never assured, investors’ odds improve over longer time horizons.

Conclusion

While some investors might find it easy to stay the course in years with above average annual returns, periods of disappointing results may test an investor’s faith in equity markets. Being aware of the range of potential outcomes can help investors remain disciplined, which in the long term can increase the odds of a successful investment experience. What can help investors endure the ups and downs? While there is no silver bullet, having an understanding of how markets work and trusting market prices are good starting points. An asset allocation that aligns with personal risk tolerances and investment goals is also valuable. In addition, we believe that a Johns Island Financial Advisor can play a critical role in helping investors sort through these and other issues as well as keeping them focused on their long‑term goals. We’d love to get to know you; give us a call to see how we can become your trusted financial partner.

1. As measured by the S&P 500 Index from 1926–2016.

2. In US dollars. The S&P data are provided by Standard & Poor’s Index Services Group. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Index returns and average annual return do not reflect the cost associated with an actual investment.

3. From January 1926–December 2016 there are 913 overlapping 15-year periods, 973 overlapping 10-year periods, 1,033 overlapping 5-year periods, and 1,081 overlapping 1-year periods. The first period starts in January 1926, the second period starts in February 1926, the third in March 1926, and so on. In US dollars. The S&P data are provided by Standard & Poor’s Index Services Group. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not an indication of future results.

4. Source: Dimensional Fund Advisors with edits by Coastal Wealth Advisors, LLC