“Doubt is not a pleasant condition, but certainty is an absurd one.” – Voltaire

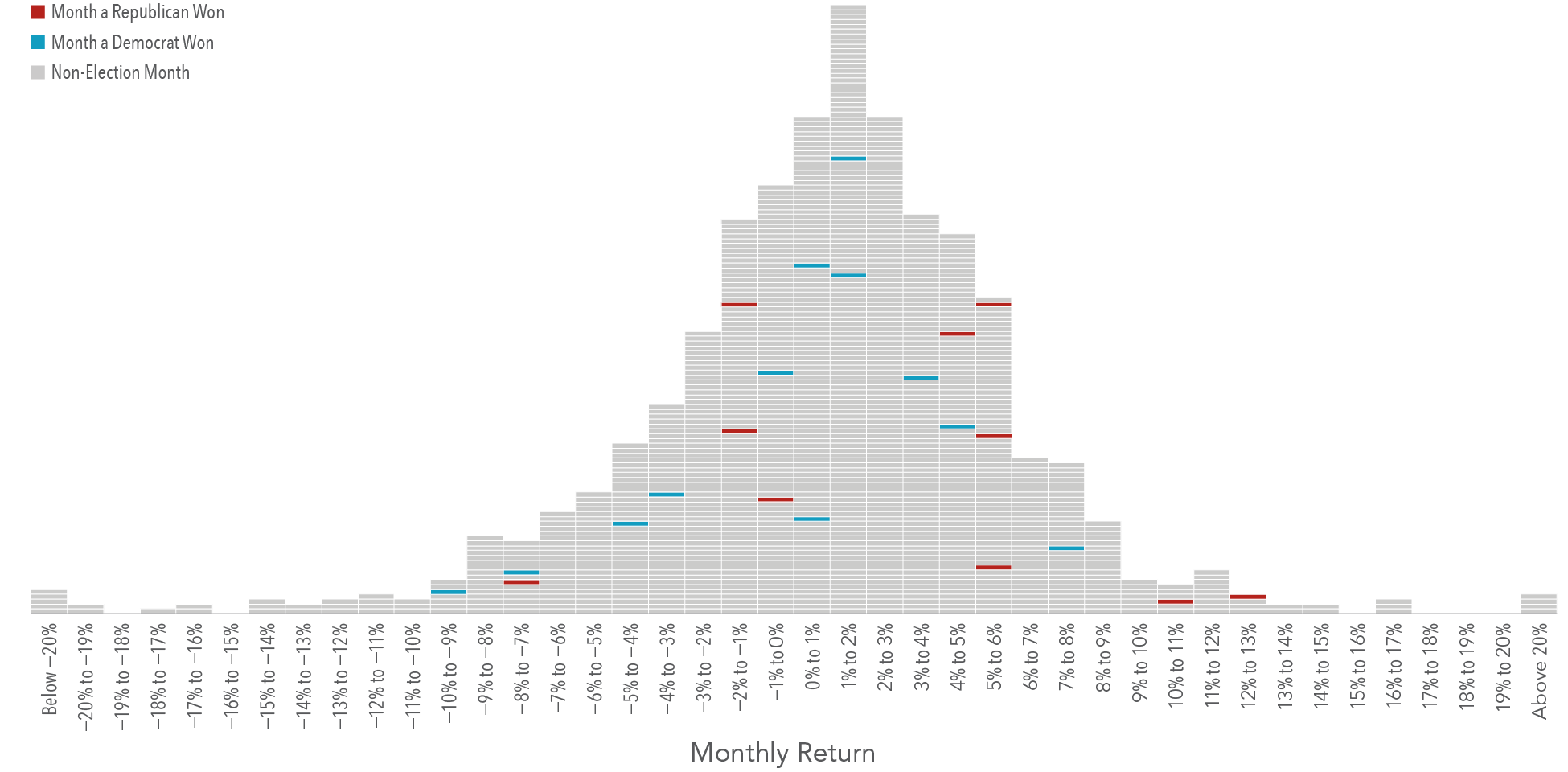

“The market hates uncertainty” has been a common enough saying in recent years, but how logical is it? There are many different aspects to uncertainty, some that can be measured and some that cannot. Uncertainty is an unchangeable condition of existence. As individuals, we can feel more or less uncertain, but that is a distinctly human phenomenon. Rather than ebbing and flowing with investor sentiment, uncertainty is an inherent and ever-present part of investing in markets. Any investment that has an expected return above the prevailing “risk-free rate” (think treasury bills for investors) involves trading off certainty for a potentially increased return.

Consider this concept through the lens of stock vs. bond investments; what we call the first premium during our portfolio reviews. Stocks have higher expected returns than bonds largely because there is more uncertainty about the future state of the world for equity investors than bond investors. Bonds, for the most part, have fixed coupon payments and a maturity date at which principal is expected to be repaid. Stocks have neither. Bonds also sit higher in a company’s capital structure. In the event a firm goes bust, bondholders get paid before stockholders. So, do investors avoid stocks in favor of bonds as a result of this increased uncertainty? Quite the contrary, many investors end up allocating capital to stocks due to their higher expected return. In the end, many investors are often willing to make the tradeoff of bearing some increased uncertainty for potentially higher returns.

MANAGING UNCERTAINTY EMOTIONS

While the statement “the market hates uncertainty” may not be totally logical, it doesn’t mean it lacks educational value. Thinking about what the statement is expressing allows us to gain insight into the mindset of individuals. The statement attempts to personify the market by ascribing the very real nervousness and fear felt by some investors when volatility increases. In behavioral finance, we feel losses more than we feel gains. It is recognition of the fact that when markets go up and down, many investors struggle to separate their emotions from their investments. It ultimately tells us that for many an investor, regardless of whether markets are reaching new highs or declining, changes in market prices (equating to changes in your portfolio values) can be a source of anxiety.

Watch: Can you Predict a Good time to Buy Stocks?

During these periods, it may not feel like a good time to invest. Only with the benefit of hindsight do we feel as if we know whether any time period was a good one to be invested. Unfortunately, while the past may be prologue, the future will forever remain uncertain. It is without a doubt, impossible to predict if today is the highest of highs or lowest of lows. For this reason, we believe you should remain invested through all periods.

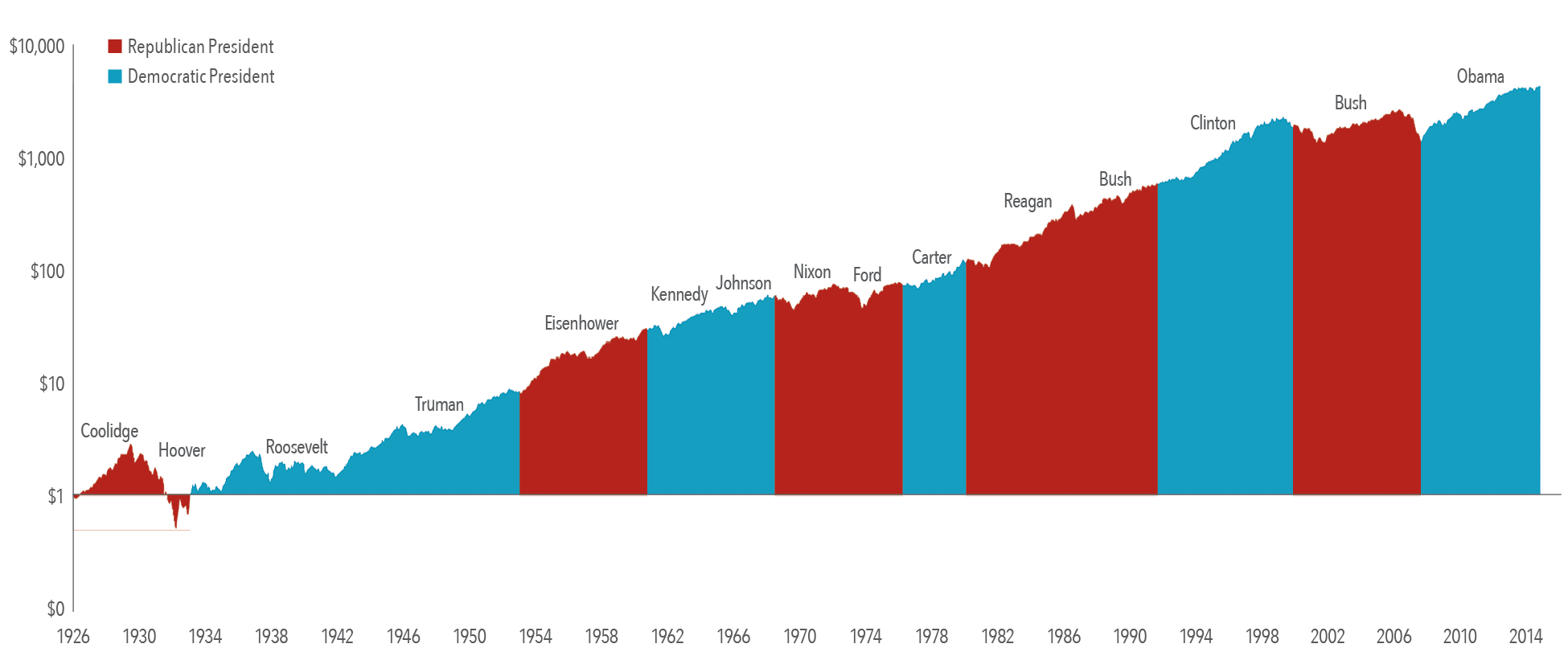

STAYING IN YOUR SEAT DURING UNCERTAINTY: HOW LONG IS LONG-TERM?

In a recent interview, Chairman of Dimensional Fund Advisors, LP (DFA Funds), David Booth, was asked about what it means to be a long-term investor:

“People often ask the question, ‘How long do I have to wait for an investment strategy to pay off? How long do I have to wait so I’m confident that stocks will have a higher return than money market funds, or have a positive return?’ And my answer is it’s at least one year longer than you’re willing to give. There is no magic number. Risk is always there.”

Part of being able to stay unemotional during periods when it feels like uncertainty has increased is having an appropriate asset allocation that is in line with an investor’s willingness and ability to bear risk. It also helps to have a partner like us who consistently monitors your portfolio Riskalyze Score to ensure it remains on course.

Remember that during what feels like good times and bad, one wouldn’t expect to earn a higher return without taking on some form of risk. How much risk to take depends solely on your financial goals. While a decline in markets may not feel good, having a portfolio you are comfortable with, understanding that uncertainty is part of investing, and sticking to a plan that is agreed upon in advance and reviewed on a regular basis can help keep investors from reacting emotionally. We believe that when you approach your wealth management with us as your partner and with this mindset, it can ultimately lead to a better investment experience.

Source: Dimensional Fund Advisors with edits by Coastal Wealth Advisors